Scale creates the surface area. Value drives the spike. From Valve’s Counter-Strike (#1, +$37.1M) to EA’s EA Sports FC (#15, +$2.1M), this month’s ALDORA leaderboard shows a consistent pattern: revenue increases concentrate around moments that give players a reason to spend.

ALDORA tracks monthly revenue across mobile, Steam, and box office channels. Delta revenue reflects the month-over-month change in revenue, capturing incremental growth rather than total revenue.

Execution Over Scale

At the top of the leaderboard, execution, not just audience size, drives outcomes. Nintendo’s Pokémon (#3, +$19.4M) and Activision Blizzard’s Call of Duty (#4, +$9.1M) both benefited from strong engagement cycles that drove players to spend.

The same pattern holds at #1. Counter-Strike didn’t lead on scale alone. It benefited from a clear reactivation moment that translated directly into revenue. Meanwhile, Apex Legends (#2) shows how consistent update cadence can sustain monetization over time.

Revenue Is a Function of Cadence

Further down the leaderboard, cadence remains a key driver. Ubisoft appears twice with Rainbow Six (#5, +$6.1M) and Assassin’s Creed (#9, +$3.8M), reflecting ongoing live activity on Steam. While not indicative of broader company performance, both franchises show how consistent updates can still generate incremental revenue gains.

Bandai Namco Entertainment’s Dragon Ball (#6, +$4.8M) and Hasbro’s Dungeons & Dragons (#7, +$4.5M) reflect structured content strategies, but their placement also highlights how effectively that engagement translates into measurable spending.

CD Projekt’s Cyberpunk (#10, +$3.3M) saw a lift aligned with broader distribution changes, while MLB (#11, +$3.3M) benefited from seasonal timing. These are clear inflection points that drove spending and leaderboard movement.

Different Paths, Same Outcome

The rest of the leaderboard highlights how diverse revenue drivers can be. Capcom’s Resident Evil (#12, +$2.6M) leveraged its 30th anniversary, while Stardew Valley (#13, +$2.4M) continues to benefit from momentum carried over from its 10th anniversary celebrations in February, compounding through ongoing updates and sustained community engagement. Shueisha’s Demon Slayer (#14, +$2.2M) and Electronic Arts’ EA Sports FC (#15, +$2.1M) round out the list, showing that even smaller revenue gains are tied to deliberate product and content decisions.

The winners are those who convert attention into spending. The ALDORA leaderboard captures those moments in real time.

ALDORA tracks brand performance across five dimensions of the gaming ecosystem—Play (direct gameplay), Watch (streaming and video content), Connect (social interactions), Create (user-generated content), and Spend (in-game purchases and merchandise)—linking engagement signals directly to revenue outcomes.

KEY INSIGHTS

1. Scale ≠ Revenue

Counter-Strike (#1, +$37.1M) and Apex Legends (#2, +$25.1M) didn’t lead because they’re big; they led because they gave players a reason to spend. Scale created the opportunity. Value—and execution—drove the outcome.

2. Cadence Drives Monetization

From Call of Duty (#4, +$9.1M) to Rainbow Six (#5, +$6.1M), spikes in revenue growth are tied to updates, seasonal drops, and structured content roadmaps. Cadence isn’t just a retention tool; it’s a monetization strategy. Publishers who ship on a rhythm give players a recurring reason to spend.

3. Revenue Is Event-Driven

From Cyberpunk (#10, +$3.3M) to MLB (#11, +$3.3M), revenue growth clusters around key moments. These are inflection points. The franchises that plan for them capture the spend; the rest miss it.

Analysis by ALDORA CEO Joost van Dreunen

Contact

ALDORA

🌐 www.aldora.io

📍 Brooklyn, NY

ALDORA Leaderboard: Reach Precedes Revenue March 2026

Big audiences are easy to overread. Barbie leads at #1 with 53.6 million reach, and Hasbro’s Dungeons & Dragons sits at #7 with 31.7 million. But the leaderboard isn’t just a ranking—it’s a measure of how attention spreads across franchises, from blockbuster hits to evergreen and niche titles, and which companies are positioned to put that attention to work.

Barbie’s reach still carries the long tail of a rare cultural moment. The 2023 film left such a massive footprint that its effects continue to shape visibility today. That does not make the audience any less real, but it does sharpen the strategic question: can Mattel convert residual cultural relevance into recurring digital engagement?

Infrastructure Is the Real Differentiator

Hasbro is already ahead on that front. Following February’s earnings, investors focused on its digital gaming business, sending the stock up 9%. The company has built the infrastructure to turn engagement into revenue. Mattel is now following a similar path, committing $110 million to digital gaming in 2026 and $40 million in performance marketing. That strategy is already taking shape: Mattel recently acquired full ownership of Mattel163, its mobile games studio with over 550 million downloads and 20 million monthly active users. Even attention inherited from a major media moment can become a fully integrated digital business—if the strategy is in place.

Leaderboard Patterns Across Franchises

The rest of the leaderboard highlights different engagement patterns across franchises. Disney dominates numerically with #2 Marvel (53.3M), #5 Spider-Man (36.5M), #6 Avatar (33.5M), and #11 Star Wars (28.2M), showing the scale of a diversified IP portfolio—and the challenge of maintaining engagement across multiple franchises. Evergreen franchises like #3 Minecraft (49.2M) sustain massive reach through ongoing engagement, while legacy IPs such as #4 Jurassic Park (45.8M), #9 Batman (30.7M), and #12 Sonic the Hedgehog (27.8M) maintain solid footprints even without new releases. Smaller, digitally-native hits like #14 Hollow Knight (23.9M) and #15 Demon Slayer (22.4M) prove that passionate niche communities can punch far above their weight.

Across categories, one pattern is clear: reach does not automatically translate to financial success. Movies spike and fade, games compound over time, and portfolio IP spreads attention across channels. The leaderboard captures where audiences are—but the real question is what comes next. Mattel has the audience. Hasbro has shown the blueprint for conversion. The next phase will be about turning attention into lasting value.

ALDORA tracks brand performance across five dimensions of the gaming ecosystem—Play (direct gameplay), Watch (streaming and video content), Connect (social interactions), Create (user-generated content), and Spend (in-game purchases and merchandise)—aggregating these diverse engagement signals into a unified measure of audience reach.

KEY INSIGHTS

1. Reach ≠ Revenue

Barbie leads the leaderboard at #1 with 53.6M reach, while Dungeons & Dragons sits at #7 with 31.7M. Large audiences indicate attention, but converting that attention into digital engagement or revenue requires infrastructure, strategy, and execution.

2. Digital infrastructure amplifies engagement

Hasbro’s digital gaming business drove a 9% post-earnings stock uptick, showing how digital infrastructure supports audience engagement. Mattel is following suit with $110M in digital gaming and full ownership of Mattel163, which reaches 20M monthly active users.

3. Scale Across Franchises

Disney makes commanding large audiences across multiple franchises look easy. Marvel (#2, 53.3M), Spider-Man (#5, 36.5M), Avatar (#6, 33.5M), and Star Wars (#11, 28.2M) show how a diversified IP portfolio spreads attention across several hits, while smaller franchises like Hollow Knight (#14, 23.9M) and Demon Slayer (#15, 22.4M) demonstrate the impact of niche, highly engaged audiences.

Eager for next month’s leaderboard? Follow ALDORA on LinkedIn to be the first to see where culture, capital, and consumer power collide next.

Analysis by ALDORA CEO Joost van Dreunen

Contact

ALDORA

🌐 www.aldora.io

📍 Brooklyn, NY

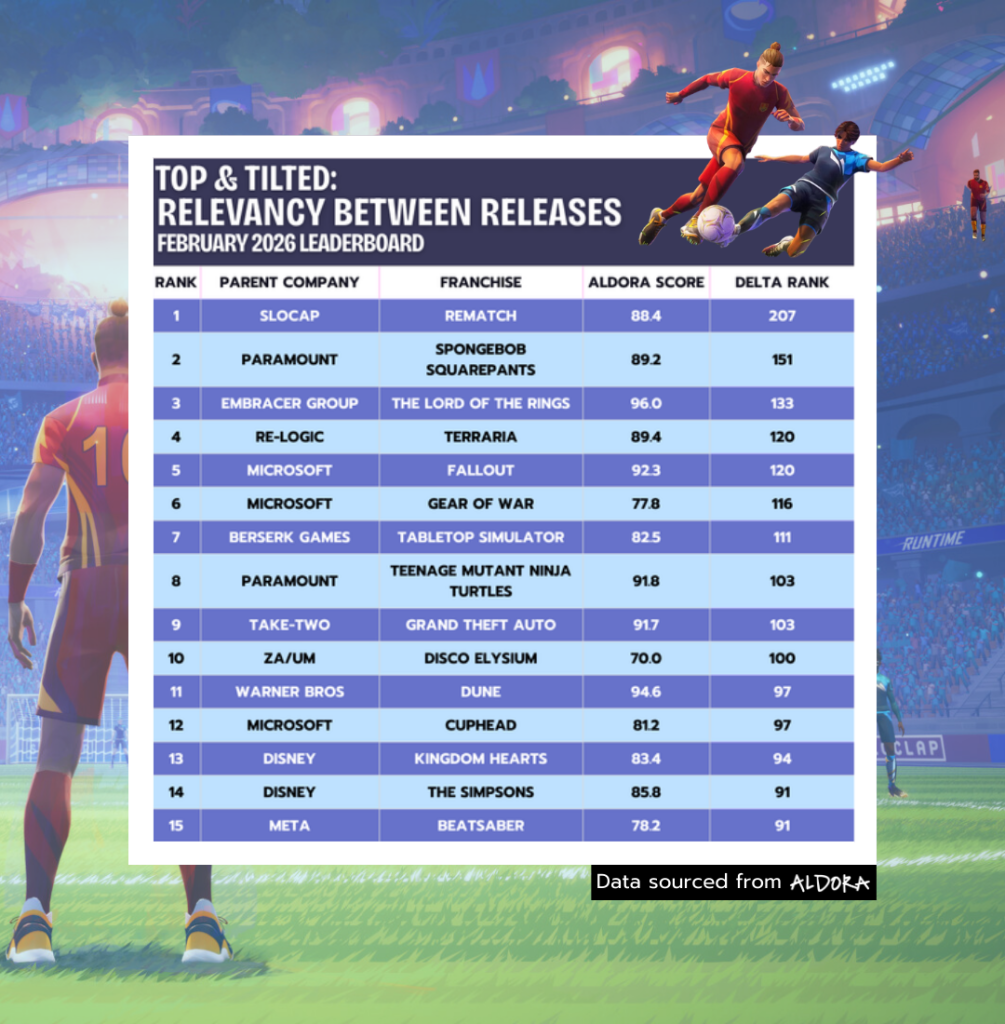

ALDORA Leaderboard: Relevancy Between Releases February 2026

ALDORA’s first set of 2026 data is already revealing a defining shift in franchise competition: the most momentous franchises no longer rely on major launches to sustain cultural and commercial relevance. Today, even seemingly small touchpoints can generate meaningful momentum, proving that true franchise strength is defined by who wins between releases.

This month’s strongest performers climbed the charts through continuous lifecycle touchpoints, not one-off releases. And while the industry still celebrates milestone launches, audiences reward persistent presence—sustained through updates, anniversaries, revivals, and cross-platform engagement that keeps franchises culturally and commercially relevant between major content drops.

About this month’s leaderboard: February’s rankings are based on January data and focus specifically on trending franchises, or those exhibiting the greatest positive month-over-month rank movement relative to the prior period.

Leaderboard Terms:

ALDORA Score: A normalized monthly score (0–100) that ranks franchises based on aggregated performance across five behavioral dimensions: Play, Watch, Connect, Create, and Spend.

Delta Rank: The net change in position across all five behavioral dimensions, capturing the overall directional shift in franchise engagement rather than isolated category movement.

REMATCH (#1) leads this month’s trending leaderboard with an ALDORA Score of 88.4 and a Delta Rank of 207. Following its December release of season two, developer Slocap sustained engagement through rapid fix updates and live-service improvements. Its performance reinforces a broader structural shift in gaming: launch windows now serve as entry points rather than peak-engagement moments. REMATCH’s continued upward movement demonstrates how post-release iteration and community responsiveness can drive sustained momentum well beyond initial launch cycles.

Paramount’s SpongeBob SquarePants (#2) posts an ALDORA Score of 89.2 and a Delta Rank of 151 following the digital release of its latest film sequel on January 20. The franchise continues to demonstrate rare cross-generational staying power across streaming, merchandise, gaming, and creator ecosystems. Bonus content—such as an Ice Spice music video—signals how music and creator partnerships are becoming core tools for sustaining franchise relevance.

Embracer Group’s The Lord of the Rings (#3) leads this month with the highest ALDORA Score at 96 and a Delta Rank of 133. The franchise’s 25th-anniversary theatrical re-release demonstrates how legacy IP can re-engage audiences through strategic rediscovery. LOTR continues to exemplify how franchise capital compounds, with each revival expanding engagement across viewing, fandom, and merchandise.

Elsewhere on the leaderboard, community-driven and live-service platforms continue to demonstrate durable engagement patterns. Terraria (#4, 89.4 ALDORA Score, 120 Delta Rank) surged following the release of its major 1.4.5 “Bigger & Boulder” update, showcasing how developer commitment to post-launch support sustains long-tail player investment. Similarly, Tabletop Simulator (#7, 82.5, 111 Delta Rank) benefits from announced platform improvements that reinforce its role as an evergreen creator and social play environment.

Microsoft’s franchise portfolio demonstrates ecosystem-level orchestration across multiple properties this month. Fallout (#5, 92.3, 120 Delta Rank) gained momentum through Xbox Free Play Days for Fallout 76 alongside community-generated content expansion for Fallout 4. Meanwhile, Gears of War (#6, 77.8, 116 Delta Rank) rose on confirmation of its 2026 release, proving that signaling future content can be as powerful as launching it. Cuphead (#12, 81.2, 97 Delta Rank) reinforces the publisher’s ability to maintain engagement across stylistically distinct properties that sustain both nostalgic and creator-driven participation.

Paramount appears again with Teenage Mutant Ninja Turtles (#8, 91.8, 103 Delta Rank), supported by the announcement of a second season of Tales of the Teenage Mutant Ninja Turtles. The franchise’s consistent cross-format storytelling reinforces Paramount’s expanding ability to transform legacy animation IP into multi-surface engagement ecosystems.

Take-Two’s Grand Theft Auto (#9, 91.7, 103 Delta Rank) continues to benefit from sustained player engagement and social visibility, underscoring Rockstar’s longstanding strength in maintaining cultural relevance between major franchise entries.

Legacy IP revival continues to be a powerful driver of engagement across entertainment. Warner Bros.’ Dune (#11, 94.6, 97 Delta Rank) surged following the announcement of its next film release date, while Disney’s Kingdom Hearts (#13, 83.4, 94 Delta Rank) leveraged collectible merchandise activation through a limited-edition Keyblade pin series. The Simpsons (#14, 85.8, 91 Delta Rank) similarly demonstrates how long-running franchises can sustain attention through predictive cultural commentary and social discourse.

Independent and community-driven storytelling continues to shape cultural momentum. ZA/UM’s Disco Elysium (#10, 70, 100 Delta Rank) saw renewed engagement following announcements surrounding new creative leadership developments and progress across Disco-inspired narrative RPG projects, highlighting how creator-driven narrative IP can sustain relevance through development visibility and community interest. Meta’s Beat Saber (#15, 78.2, 91 Delta Rank) continues to benefit from expanding VR participation and deeply entrenched user-generated content ecosystems.

Collectively, this month’s leaderboard exposes a fundamental rule change in franchise competition. Launches don’t exclusively drive success. Momentous participation ecosystems do. Today, launches are sparks. The real winners are the ones who keep the fire burning.

ALDORA tracks brand performance across five dimensions of the gaming ecosystem—Play (direct gameplay), Watch (streaming and video content), Connect (social interactions), Create (user-generated content), and Spend (in-game purchases and merchandise)—aggregating these diverse engagement signals into a unified measure of audience reach.

KEY INSIGHTS

1. The lifecycle has replaced the launch as gaming’s primary growth engine.

February’s leaderboard reinforces a structural shift in how franchises build and sustain momentum. Slocap’s REMATCH (#1, 88.4, 207 Delta Rank) continues growing post-launch with iterative updates, Re-Logic’s Terraria (#4, 89.4, 120 Delta Rank) surged following the “Bigger & Boulder” update, and Microsoft’s Fallout (#5, 92.3, 120 Delta Rank) leveraged Free Play Days and new community content to re-engage audiences. These examples demonstrate that competitive advantage increasingly accrues to franchises that operate as ongoing services.

The industry historically optimized for momentary demand spikes. Audiences now reward continuous relevance. The franchises that win are those that consistently create reasons to return, participate, and contribute.

2. Franchise value no longer decays between releases. It compounds through revival cycles.

The performance of Embracer Group’s The Lord of the Rings (#3, 96, 133 Delta Rank), Warner Bros’ Dune (#11, 94.6, 97 Delta Rank), Paramount’s SpongeBob SquarePants (#2, 89.2, 151 Delta Rank), Paramount’s Teenage Mutant Ninja Turtles (#8, 91.8, 103 Delta Rank), and Disney’s Kingdom Hearts (#13, 83.4, 94 Delta Rank) demonstrates how legacy franchises continue to accumulate cultural and commercial capital through strategic reintroductions, anniversary programming, merchandise activation, and streaming distribution.

Rather than fading between installments, these franchises monetize familiarity and emotional continuity. Legacy IP increasingly behaves like an annuity stream, where each revival reactivates dormant audiences while onboarding new generations across platforms and formats.

3. Ecosystem orchestration is overtaking single-IP strategy as the dominant competitive advantage.

Microsoft’s multi-franchise footprint (Fallout, Gears of War #6, 77.8, 116 Delta Rank, Cuphead #12, 81.2, 97 Delta Rank) illustrates how platform operators can sustain engagement through coordinated portfolio management across distinct IP. Simultaneously, community-driven ecosystems such as Terraria, Tabletop Simulator (#7, 82.5, 111 Delta Rank), Disco Elysium (#10, 70, 100 Delta Rank), and Beat Saber (#15, 78.2, 91 Delta Rank) demonstrate that creator participation, modding culture, and social play loops can rival traditional marketing scale in sustaining long-term engagement.

The competitive battleground is shifting from content ownership to audience orchestration. The organizations that connect play, viewing, creation, identity, and commerce into unified behavioral systems will define the next franchise leaders.

Attention is fleeting. Participation is power. Franchises that maintain touchpoints between releases turn both into enduring cultural gravity, and tomorrow’s winners will be those who never stop engaging.

Eager for next month’s leaderboard? Follow ALDORA on LinkedIn to be the first to see where culture, capital, and consumer power collide next.

Analysis by ALDORA CEO Joost van Dreunen

Contact

ALDORA

🌐 www.aldora.io

📍 Brooklyn, NY

ALDORA Leaderboard: Ubiquity Begets Success January 2026

ALDORA’s final data for 2025 show that at the close of the year, the most successful brands and franchises are the ones that have successfully established themselves across different channels for interaction and engagement with audiences. In December 2025, franchises competed for holiday attention as gifting cycles, increased downtime, and shared viewing converged. The winners weren’t simply those with the best content, merchandise, or social presence—they were the ones operating as full-scale ecosystems.

About this month’s leaderboard: January’s rankings are based on December data and focus on trending franchises, or those exhibiting the greatest positive month-over-month rank change relative to the prior period.

Leaderboard Terms:

ALDORA Score: A normalized monthly score (0–100) that ranks franchises based on aggregated performance across five behavioral dimensions: Play, Watch, Connect, Create, and Spend.

Momentum Index: A composite measure of net rank movement across the same five behavioral dimensions, capturing overall directional momentum rather than isolated changes within any single category.

With a third film surpassing a $1B box office, it’s no surprise that Avatar (#1) leads this month’s rankings. Receiving an ALDORA Score of 90 and a Momentum Index of 240, not only did Avatar generate a massive global reach in December, but it also accelerated engagement across gaming, video, social, and commerce.

LEGO (#2) follows with an ALDORA Score of 81.7 and a Momentum Index of 171, reinforcing its position as one of the world’s top franchises and cultural touchstones, spanning physical play, user-generated creation, licensed games, and global media presence.

Following the theatrical release of its sequel, Five Nights at Freddy’s (#3) posts an 87.7 ALDORA Score and 167 Momentum Index, demonstrating how creator-driven fandoms and transmedia storytelling can rival the scale of traditional entertainment giants.

Together, the top three illustrate a broader structural shift: franchises that orchestrate interaction across films, games, merchandise, creator platforms, and social ecosystems compound faster and more durably than those competing solely for passive or single-format attention. It’s one thing to attract audiences, and another to effectively activate them.

Additionally, persistent, community-driven platforms like Destiny (89.4 score), No Man’s Sky (83.3), Dungeons & Dragons (91.7), and emerging live-service contenders like REMATCH (81.8) demonstrate resilient engagement. Meanwhile, revitalized legacy franchises, including Assassin’s Creed (83.5), Tomb Raider (79.9), Silent Hill (77.3), Metro (76.7), and Armored Core (61.9), which reflects renewed momentum in Bandai Namco’s legacy franchise strategy, benefit from IP refreshes but remain driven by release peaks instead of consistent activity. It’s enough to place them on this month’s leaderboard, but without a transmedia ecosystem, will they sustain meaningful momentum?

One unconventional outlier stands out. At #8, Tesla (81.1 ALDORA Score, 110 Momentum Index) sits firmly in the middle of this month’s Top & Tilted contenders. Its presence underscores how brand platforms increasingly behave like cultural ecosystems—blending identity, community participation, merchandising, and social amplification to generate persistent engagement. Even as Tesla’s Q4 2025 vehicle deliveries came in below consensus expectations, its cultural relevance remains robust through social buzz and online engagement. Tesla’s sustained attention through social discourse and online activity shows that today’s cultural relevance is driven as much by participation and visibility as by product performance.

This month’s top franchises turn attention into participation across screens, platforms, and products. The holiday window magnifies this advantage, accelerating discovery, onboarding, and cross-format migration. But the real winners don’t rely on seasonal spikes. They build enduring cultural gravity.

ALDORA tracks brand performance across five dimensions of the gaming ecosystem—Play (direct gameplay), Watch (streaming and video content), Connect (social interactions), Create (user-generated content), and Spend (in-game purchases and merchandise)—aggregating these diverse engagement signals into a unified measure of audience reach.

KEY INSIGHTS

1. Transmedia ecosystems are now the primary drivers of cultural scale.

The top of January’s leaderboard is populated by franchises that operate as integrated participation platforms rather than isolated entertainment products. Avatar (#1, 90 ALDORA Score, 240 Momentum), LEGO (#2, 81.7 Score, 171 Momentum), and Five Nights at Freddy’s (#3, 87.7 Score, 167 Momentum) all activate and engage audiences across film, gameplay, physical products, creator ecosystems, and social engagement.

These leaders are distinguished by their velocity. Their elevated Momentum Index reflects magnifying behavior: fans migrate between formats, participate through creation, play, and community that sustains even between major releases. The implication is structural. Cultural power is increasingly determined by how well a franchise organizes participation across surfaces, rather than how successfully it launches a single product.

2. Participation-first platforms demonstrate stronger resilience than release-driven franchises.

Beyond the top three, participation-driven worlds continue to demonstrate durable engagement profiles. Destiny (89.4), No Man’s Sky (83.3), Dungeons & Dragons (91.7), and emerging live-service contenders like REMATCH (81.8) maintain strong scores because they are built around continuous interaction, community identity, and long-tail content cycles.

These platforms benefit more from retained behavior loops than from seasonal volatility: live updates, social coordination, creator ecosystems, and sustained player investment drive ongoing engagement beyond individual release windows. Their Momentum Index performance suggests steadier engagement patterns rather than purely launch-driven spikes.

By contrast, revitalized legacy franchises, including Assassin’s Creed, Tomb Raider, Silent Hill, Metro, Armored Core, and Dune, gain from refreshed IP cycles but remain more closely tied to release peaks than to sustained ecosystem momentum. They generate meaningful bursts of attention, but their growth capacity remains structurally constrained without deeper participation layers.

3. Brand platforms increasingly behave like entertainment ecosystems.

The presence of Tesla (#8, 81.1 Score, 110 Momentum) among this month’s leaders reminds us how cultural platforms are no longer confined to traditional media categories. Tesla’s engagement profile reflects many of the same dynamics as top franchises: identity signaling, community participation, merchandise demand, creator amplification, and persistent social visibility. Even amid softening sales momentum, Tesla sustains cultural relevance through ongoing discourse and network effects rather than product cadence alone.

This convergence articulates a broader competitive reality: brands, IP owners, and platforms are now competing on their ability to sustain participatory ecosystems, not simply on product output.

4. The competitive battlefield is shifting from content leadership to ecosystem orchestration.

The January leaderboard illustrates the critical gap between franchises optimized for participation and those optimized for distribution. Production scale, marketing reach, or platform access alone don’t define success. Instead, the franchises on top are those that effectively connect play, viewing, creation, commerce, and community into a cohesive behavioral loop.

Avatar, LEGO, and Five Nights at Freddy’s exemplify this. Their performance reflects not just popularity, but systemic design: multiple entry points, cross-format reinforcement, and durable fan investment that intensifies over time.

As more franchises pursue transmedia expansion, execution becomes the true differentiator. Owning IP is no longer enough. The winners will be the organizations that can design, operate, and sustain ecosystems that consistently convert attention into participation—and participation into lasting cultural power.

Eager for next month’s leaderboard? Follow ALDORA on LinkedIn to be the first to see where culture, capital, and consumer power collide next.

Analysis by ALDORA CEO Joost van Dreunen

Contact

ALDORA

🌐 www.aldora.io

📍 Brooklyn, NY

ALDORA Leaderboard: Disney Commands the Holidays, Netflix Claims Its Challenger, December 2025

Report:

In November 2025, top film franchises commanded massive reach, and with Netflix now controlling Warner Bros., the balance of power in streaming is shifting fast. This month’s leaderboard highlights exactly what drew Netflix to WB: franchises with built-in reach, cultural pull, and untapped cross-platform potential—including gaming, whether they care to admit it or not.

To no one’s surprise, Disney takes the charts for early-holiday viewing with seven franchises combining for 235M reach, while Warner Bros., now under Netflix, adds 165M reach across four titles, including Superman (60M) and Barbie (55M). The $82.7 billion Warner Bros. acquisition gives Netflix immediate access to IP built not just for passive viewing, but for interactive, cross-platform expansion.

Netflix insists WB’s game studios didn’t factor into the deal. But the reality is that the IP they now hold could reshape their entire interactive strategy, assuming they address the operational hurdles they’ve faced in the past.

This month’s leaderboard speaks directly to how the biggest franchises make the most of both screens and platforms. The real winners will be the ones who can activate these worlds everywhere, from film to streaming to games. That’s exactly why Netflix’s new WB IP is so compelling.

The Breakdown

Superman (Warner Bros., 60M reach) claims the top spot this month, signalling just how potent WB’s worlds remain, even before Netflix fully integrates them. Barbie (Mattel/WB, 55M) lands at #2, proving its post-theatrical momentum hasn’t slowed. Disney follows with a barrage of heavy hitters: Inside Out (54M), Spider-Man (34M), Avatar (32M), Marvel (31M), X-Men (30M), Lion King (28M), Frozen (26M).

Nostalgia, family viewing, and emotional comfort all drive November reach, and no one monetizes that better than Disney.

But the leaderboard also exposes the next competitive fault line: franchises built to be interacted with.

Minecraft (31M), Sonic the Hedgehog (25M), Jurassic Park (45M), and Mission Impossible (26M) all demonstrate strong cross-format demand with worlds that are equally at home in games, film, TV, and merchandise.

And then there’s Dune (WB, 23M). Prestige, fandom, replay value, and unmistakable gaming potential. Once Netflix begins integrating WB’s library, they’ll have all the strategic ammunition they need to claim their stake in streaming and interactive entertainment. But how that plays out depends on Netflix’s approach. Owning the IP alone won’t be enough if they don’t back it with the talent, operation, and strategy it requires to take it the distance.

ALDORA tracks brand performance across five dimensions of the gaming ecosystem—Play (direct gameplay), Watch (streaming and video content), Connect (social interactions), Create (user-generated content), and Spend (in-game purchases and merchandise)—aggregating these diverse engagement signals into a unified measure of audience reach.

KEY INSIGHTS

1. Disney’s grasp on early holiday viewing holds strong. But Netflix’s new contender shifts the scales.

Disney claims five of the top 11 spots, with Inside Out (54M), Spider-Man (34M), and Avatar (32M) still functioning as reliable holiday performers. Their depth of family-friendly franchises continues to give them a seasonal advantage.

But the real headline is at No. 1: Superman pulls 60M, instantly becoming Netflix’s crown jewel now that the WB catalog sits under its umbrella. The acquisition hands them a top-tier franchise that rivals all of Disney’s heavy hitters.

2. IP strength is still the primary driver of reach. And Netflix now controls IP built for multi-format expansion.

Across the leaderboard, one pattern holds: The biggest numbers come from universes that already succeed across formats, including film, television, and games.

Examples:

- Minecraft (31M) continues to prove the power of game-native IP to cross media boundaries.

- Sonic (25M) remains Sega’s multimedia performance powerhouse.

- Superman (60M) demonstrates how legacy world-building drives both viewership and long-term engagement.

Netflix spent years trying to build original gaming traction from scratch. Now they suddenly own franchises with decades of lore, fan identity, and gameplay precedent. That fundamentally changes their strategic advantage.

3. Netflix says WB’s game studios didn’t factor into the acquisition. But is that the truth?

Publicly, Netflix maintains that gaming was incidental to the deal. But look at the numbers:

- Four of the top 15 titles (Superman, Batman, Dune, plus WB-owned DC universe) are franchises with active or historically strong game presences.

- The highest-reach franchise of the month (60M) is also one with a long history in interactive media.

- WB’s studios already produce some of the most commercially successful action RPGs of the last decade.

To say gaming “didn’t factor in” is like saying Minecraft’s 31M monthly viewers are irrelevant to Microsoft’s transmedia play. And, with data showing that 51% of Netflix subscribers have already tried Netflix Games, ignoring the potential would be a monumental misstep.

4. Netflix’s new IP amplifies the stakes across formats.

Disney still leads in sheer quantity, but Netflix now holds what it previously lacked: franchises with built-in interactive value and the potential to reach even larger audiences thanks to WB’s established film slate. Superman (60M) and Batman (29M) already show stronger game potential than most of Disney’s roster. Netflix’s existing game investments—small, scattered, underpowered—now have a north star.

As these WB films roll out on Netflix, audience reach will likely expand dramatically, shifting the competitive balance. If Netflix leverages this IP for interactive extensions, it doesn’t just compete with Disney in streaming—it challenges Microsoft, Sony, and others across culture-shaping ecosystems.

Sure, Netflix can keep saying gaming didn’t matter. But the leaderboard reveals the greater story: Superman, Barbie, Batman, and Dune are franchises designed to move across screens, and now, they’re under Netflix’s control. The opportunity is right there, in plain sight, and the question isn’t if Netflix will act—it’s how fast…and how well.

Who will take the lead next month? Follow ALDORA on LinkedIn to see where culture, capital, and consumer power collide next.

Analysis by ALDORA CEO Joost van Dreunen

Contact

ALDORA

🌐 www.aldora.io

📍 Brooklyn, NY

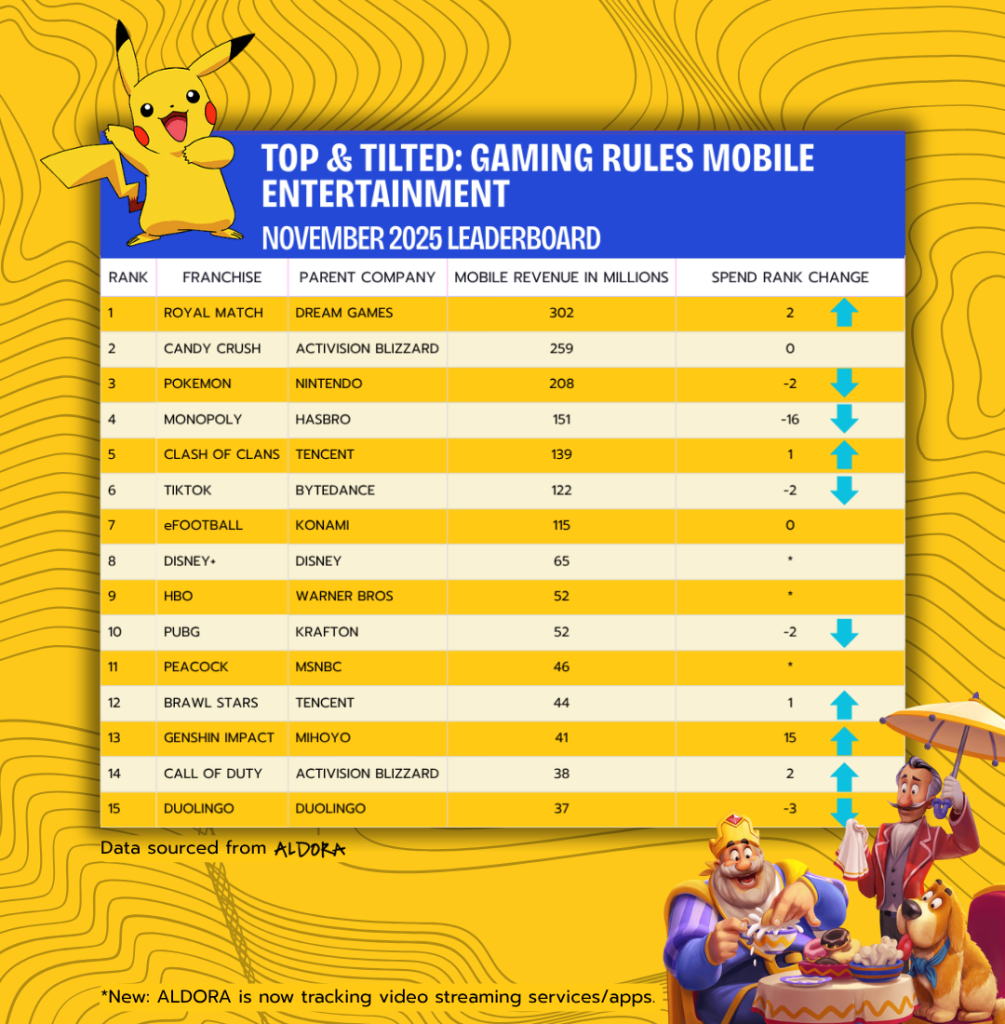

ALDORA Leaderboard: Gaming Rules Mobile Entertainment, November 2025

Report:

In October 2025, mobile spend across the top 15 franchises surpassed $1.5 billion. Mobile gamers accounted for a staggering 81% of that spend—proof that mobile is more than just a platform; it’s where culture, capital, and consumer power converge. Curious about the numbers? We’ve got them.

This month’s leaderboard signals a fundamental shift in consumer behavior: audiences are moving toward experiences where they can play, connect, and interact—not just passively watch. And they’re putting their money where their time is, proving that interactive entertainment outpaces streaming in both cultural influence and monetization.

The Breakdown

Royal Match (Dream Games) earned the #1 spot this month with $302M, up two rankings from last month. Candy Crush (Activision Blizzard, $259M) and Pokémon (Nintendo, $208M) rounded out the top three, demonstrating that classic IP still holds immense sway over audiences and their wallets. Tencent’s Clash of Clans ($139M) and Brawl Stars ($44M) also climbed the ranks, reinforcing that live-service, community-driven models turn engagement into sustainable capital.

Meanwhile, narrative-rich, globally accessible games are rising faster than ever: Genshin Impact ($41M) surged 15 spots to claim a top position on the leaderboard, proving that strong storytelling can convert audiences into paying, loyal communities even on mobile-first platforms.

Streaming platforms like Disney+ ($65M), HBO ($52M), and Peacock ($46M) continued to capture audience attention, but their mobile revenue lags behind that of interactive franchises. Unlike games, where engagement drives ongoing purchases, streaming revenue is largely passive and subscription-based. This gap spotlights a critical trend: in mobile entertainment, engagement drives both culture and cash flow.

ALDORA tracks brand performance across five dimensions of the gaming ecosystem—Play (direct gameplay), Watch (streaming and video content), Connect (social interactions), Create (user-generated content), and Spend (in-game purchases and merchandise)—aggregating these diverse engagement signals into a unified measure of audience reach.

KEY INSIGHTS

Mobile IP Is the New Economic Engine.

Franchises like Royal Match ($302M), Candy Crush ($259M), and Pokémon ($208M) prove that well-designed mobile experiences can out-earn even the biggest streaming giants. Royal Match’s rise two ranks this month signals momentum, not luck, while Candy Crush and Pokémon show the enduring power of legacy IP to capture both engagement and spend.

Live-Service Communities Drive Revenue.

Clash of Clans ($139M) and Brawl Stars ($44M) illustrate how community investment translates directly into monetization. Players spend on cosmetic items, progression, and collaboration—and live-service ecosystems amplify that behavior.

Global, Narrative-Driven Titles Are the Future.

Genshin Impact’s ($41M) 15-spot jump shows that high-quality, story-driven mobile games can reach mass audiences and generate real economic impact.

Legacy IP Remains a Strategic Asset.

Classic franchises like Pokémon ($208M) and Candy Crush ($259M) remind the industry that retention, updates, and cross-promotional strategies still command serious engagement and revenue.

This month’s leaderboard confirms a new reality: spend follows engagement, and mobile is the battlefield where cultural relevance meets economic power.

Who will dominate next month? Follow ALDORA on LinkedIn to see where culture, capital, and consumer power collide next.

Analysis by ALDORA CEO Joost van Dreunen

Contact

ALDORA

🌐 www.aldora.io

📍 Brooklyn, NY

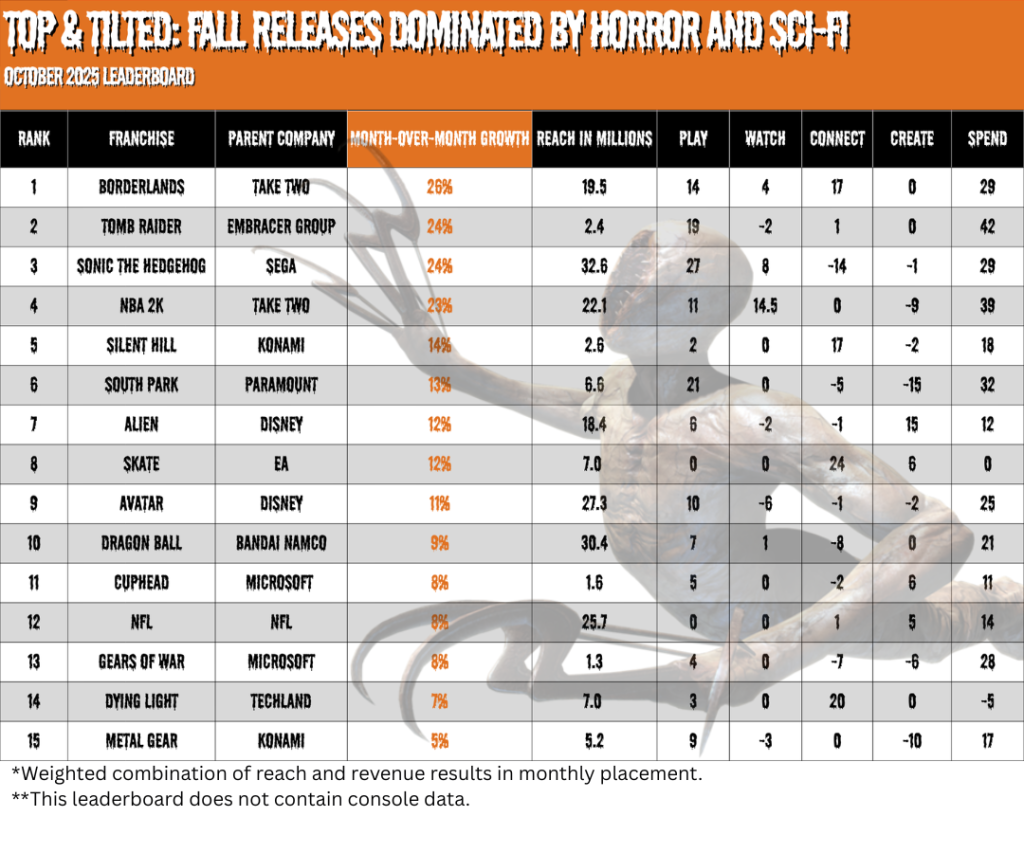

ALDORA Leaderboard: Horror and Sci-Fi Dominate Fall, October 2025

In September 2025, the audience for entertainment-based properties reached over 200 million across all forms of engagement—confirming audiences’ continued hunger for dark, high-concept worlds. Borderlands (19.5M) topped the leaderboard with a 26% month-over-month rise, driven by the release of its latest installment, Borderlands 4. Tomb Raider (+24.5%) and Sega’s Sonic the Hedgehog (+24%) followed close behind, signaling strong audience appetite for reimagined classics that merge nostalgia with fresh interactive formats.

Sports titles like NBA 2K (22.1M) and the NFL (25.7M) remained consistent cultural anchors through seasonal engagement and community participation. Meanwhile, horror and sci-fi IPs such as Silent Hill (+14%) and Alien (+12%) continued their momentum, reflecting a broader audience fascination with darker, narrative-driven experiences.

Notably, Dragon Ball (30.4M) sustained its crossover dominance, balancing anime fandom with interactive engagement, while Metal Gear and Gears of War signaled early revival energy as interest in tactical action games rebounds.

This month’s ALDORA leaderboard showcases the recession-proof qualities of the horror and sci-fi genres, which drive social and monetary engagement. As the season turns, those who can deliver psychologically twisted, grotesque, and chilling experiences rise to the top of the charts.

ALDORA tracks brand performance across five dimensions of the gaming ecosystem—Play (direct gameplay), Watch (streaming and video content), Connect (social interactions), Create (user-generated content), and Spend (in-game purchases and merchandise)—aggregating these diverse engagement signals into a unified measure of audience reach.

KEY INSIGHTS

Horror and Sci-Fi Are Driving Premium Engagement.

Five of this month’s top performers—Silent Hill (+14%), Alien (+12%), Dying Light (+7%), Sonic the Hedgehog (+24%), and Avatar (+11%)—underscore how dark, high-concept worlds command sustained attention. These franchises may not always top for reach, but they consistently overindex in play and connect behaviors, signaling deeper audience investment. Horror and sci-fi players don’t just show up—they stay, replay, and discuss.

Nostalgia Is a Growth Engine for Genre IP.

Legacy titles are proving that emotional continuity drives growth as effectively as novelty. Silent Hill’s 14% rise and Gears of War’s 8% growth show how modern reboots and remasters reignite dormant fan bases. These IPs succeed not by chasing new audiences but by reactivating long-standing communities—turning collective memory into measurable momentum.

Sci-Fi Worlds Enable Ecosystem Expansion.

Alien (+12%) and Avatar (+11%) illustrate how sci-fi IP functions as multi-format platforms rather than one-off releases. Their expansive worldbuilding enables fans to fluidly move between play, watch, and connect behaviors. With Alien gaining in create (+15) and Avatar maintaining broad reach (27.3M), both prove the scalability of transmedia storytelling.

Genre Depth Beats Mass Appeal.

While mainstream IPs like NBA 2K (+23%, 22.1M reach) dominate in scale, genre-driven franchises such as Silent Hill (+14%) and Dying Light (+7%) demonstrate deeper engagement per user. Despite their smaller audiences—2.6M and 7M respectively—both titles show strong connect activity (+17 and +20), signaling tighter, more participatory communities. These properties trade mass visibility for intensity, offering a model for sustainable fan economies as attention continues to fragment across platforms.

Legacy IP Is Finding New Life Through Interaction.

Once confined to linear formats, classic franchises are thriving through interactivity. Silent Hill’s return as an interactive narrative, Alien’s expansion into serialized streaming, and Sonic the Hedgehog’s cross-platform growth (+24%)—including brand partnerships with the Olympics and Waze—all point to a single trend: nostalgia is no longer static; it’s participatory.

Who will top—or drop from—next month’s ALDORA Leaderboard? Stay tuned to find out.

Analysis by ALDORA CEO Joost van Dreunen

Contact

ALDORA

🌐 www.aldora.io

📍 Brooklyn, NY

Top & Tilted: The Divide Between Attention and Engagement, September 2025

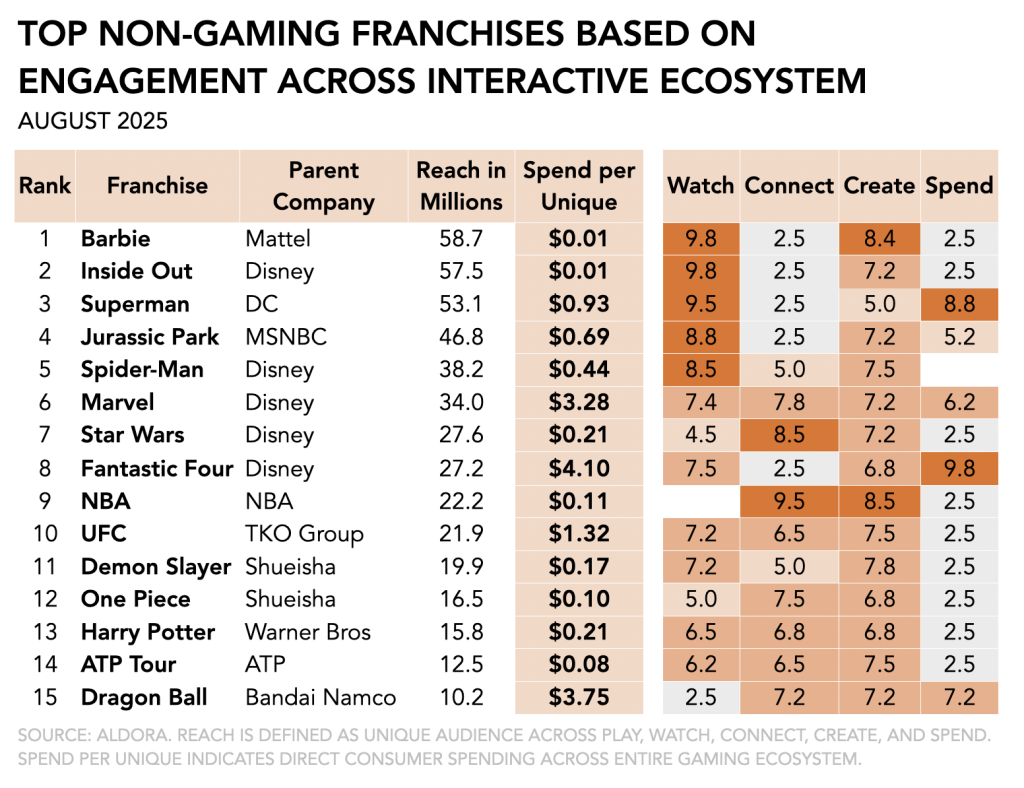

Interactive entertainment properties engaged more than 500 million unique fans in August 2025, with anime and comic franchises showing the strongest balance of cultural reach and participatory depth. Barbie (58.7 million) and Inside Out (57.5 million) led in raw visibility, but Dragon Ball (27.9 million) and Marvel’s Fantastic Four (27.2 million) proved far more effective at converting audiences into meaningful interaction and spending. Sports franchises like the NBA (22.2 million) remained cultural anchors through community connection, while legacy Hollywood IPs like Jurassic Park (46.8 million) and Harry Potter (42.3 million) struggled to move beyond passive reach.

This month’s ALDORA Leaderboard reflects a widening divide between franchises that merely attract attention and those that transform fandom into active, multi-dimensional engagement.

ALDORA tracks brand performance across five dimensions of the gaming ecosystem—Play (direct gameplay), Watch (streaming and video content), Connect (social interactions), Create (user-generated content), and Spend (in-game purchases and merchandise)—aggregating these diverse engagement signals into a unified measure of audience reach.

KEY INSIGHTS

Reach ≠ Relevance. Barbie and Inside Out topped the leaderboard in cultural footprint but converted little of their 50M+ audiences into interaction or spend. Their performance highlights the ceiling of visibility without deeper participation.

Fantastic Four Turns Fandom Into Spend. With just 27.2 million in reach, Marvel’s Fantastic Four outperformed much larger peers by posting the strongest spend-per-unique in August. The franchise illustrates how smaller but more dedicated communities can drive outsized commercial returns.

Anime Sustains Participatory Depth. Dragon Ball and One Piece continued to thrive in UGC ecosystems, where fans remix and expand worlds across play and creator platforms. Their reach may lag behind Hollywood blockbusters, but their participatory strength makes them more resilient and persistent.

Sports Anchor Culture but Lag in Spend. The NBA’s 22.2 million reach underscores its unmatched community footprint. But its monetization lags behind, with niche properties like UFC (21.9 million reach) delivering stronger spend efficiency from smaller, more passionate audiences.

Hollywood Risks “Reach Without Revenue”. Legacy franchises like Superman, Jurassic Park, and Harry Potter still command large audiences, but their inability to translate reach into interactive depth signals a fading advantage in the participatory era.

Entertainment IP now circulates through the gaming ecosystem, comprising play, watch, connect, create, and spend. The winners aren’t those who command the biggest stage, but those who inspire audiences to participate, create, and invest.

Analysis by ALDORA CEO Joost van Dreunen

Contact

ALDORA

🌐 www.aldora.io

📍 Brooklyn, NY

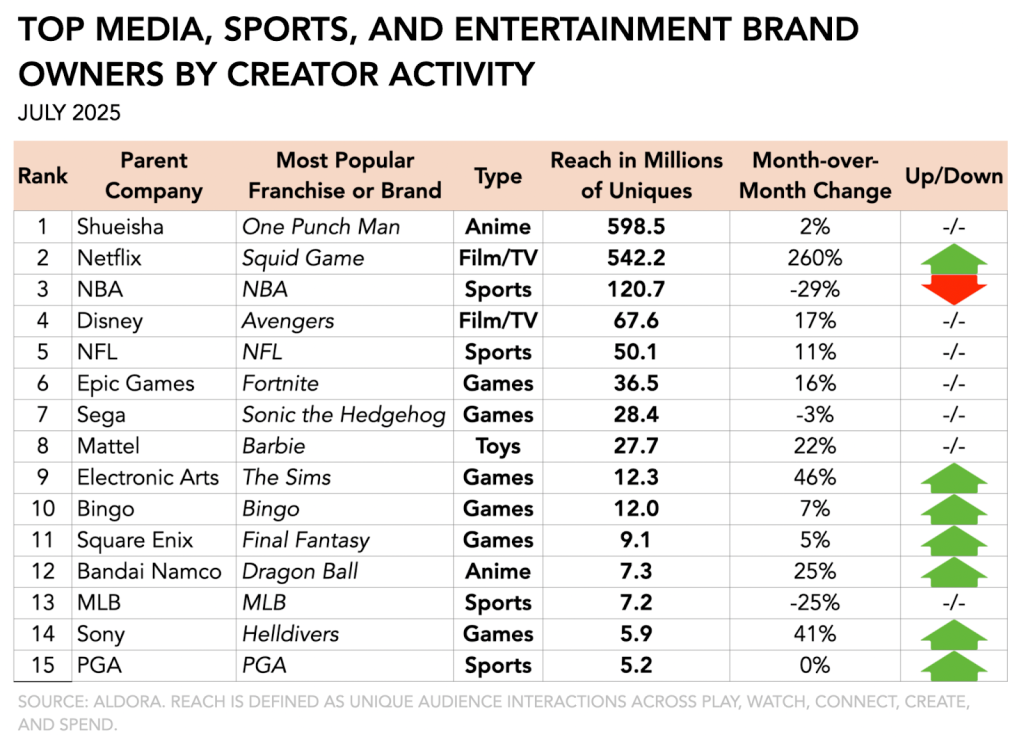

RANKED: Popularity of Media, Sports, and Entertainment Brand Owners by Creator Activity, July 2025

Interactive entertainment properties reached more than 2.1 billion unique interactions in July 2025, led by anime and streaming franchises. Anime and streaming franchises captured the top two spots for the second consecutive month, with Shueisha’s One Punch Man (598.5M interactions) and Netflix’s Squid Game (542.2M) maintaining their dominance over traditional sports properties like the NBA (120.7M, down from 170.2M in June).

This month’s ALDORA Leaderboard reflects the evolving balance of power in interactive entertainment, where global IP holders leverage gaming ecosystems to deepen cultural relevance.

ALDORA tracks brand performance across five dimensions of the gaming ecosystem—Play (direct gameplay), Watch (streaming and video content), Connect (social interactions), Create (user-generated content), and Spend (in-game purchases and merchandise)—aggregating these diverse engagement signals into a unified measure of audience reach.

KEY INSIGHTS

Participatory Entertainment Drives Growth

July’s data reiterates that cultural relevance now lives in participatory formats. The brands go beyond streaming video and passive consumption, and are remixed, role-played, and reimagined in user-generated worlds. Whether it’s fans staging their own One Punch Man battles, Squid Game’s community-built recreations, or Lady Gaga’s 591,448 concurrent players joining her Roblox appearances, growth comes from leaning into co-creation.

For brands, the strategic question is no longer how to reach audiences, but how to empower them to create alongside you.

Netflix’s Squid Game Surge Dominates

Netflix’s Squid Game delivered July’s most dramatic growth story, surging 260% from 150.6 million interactions in June to 542.2 million—catapulting from third place to second and nearly overtaking One Punch Man’s top position. Season 3, released on June 27th, delivered the franchise’s strongest interactive performance to date. For context, the season also tallied 106 million views within its first ten days, making it the most-watched in the franchise.

The brand’s ability to thrive across streaming, UGC recreations, and play environments illustrates how Netflix is evolving from passive media into participatory entertainment.

Anime Dominates User-Generated Content

One Punch Man, backed by Shueisha and distributed through Bandai Namco’s gaming arm, reached 598.5 million interactions in July, a +2 percent month-over-month gain. Remarkably, 97 percent of these took place in user-generated experiences, showing how anime fandom drives not just consumption but community creation.

Japanese publishers have perfected the anime-to-game pipeline, sustaining IP value well beyond episodic releases.

Sports Face Summer Declines

Sports properties experienced notable declines during the summer months, with the NBA dropping 29% from 170.2 million to 120.7 million interactions as the league entered its off-season. MLB saw an even steeper 25% decline from 9.6 million to 7.2 million interactions.

The NBA’s continued investment in NBA 2K (Take-Two Interactive) and Fortnite collaborations keeps it at the center of interactive fandom. Unlike episodic franchises, sports deliver predictable seasonal spikes, making leagues like the NBA indispensable cultural anchors for brands.

Entertainment IP today increasingly circulates through ecosystems of play, watch, connect, create, and spend. Winners are those who turn cultural attention into persistent, multi-platform interaction.

Analysis by ALDORA CEO Joost van Dreunen

Contact

ALDORA

🌐 www.aldora.io

📍 Brooklyn, NY

RANKED: Beauty, Retail, and Apparel, Oct 2024

Walmart leads digital engagement as beauty and retail brands see massive growth in immersive platforms versus mobile strategies.

The Short

October 2024 reveals a fascinating shift in digital engagement strategies, with traditional retailers and beauty brands showing surprising strength in immersive experiences while established apparel brands demonstrate the enduring value of mobile platforms. This month’s data highlights an evolving digital landscape where success increasingly depends on strategic platform choices rather than brand legacy alone.

Our October data reveals both established patterns and surprising disruptions in how consumers engage with brands across immersive and mobile platforms. The numbers tell a story of adaptation, innovation, and the occasional unexpected victory.

Walmart has emerged as October’s breakthrough success story, with Walmart Discovered seeing an extraordinary surge to 3.18 million new visits—more than doubling its September numbers. This immersive experience is now outperforming even its own mobile app, which recorded 1.68 million visits. With immersive engagement times averaging 7 minutes compared to 6.6 minutes on mobile, this suggests that well-crafted immersive experiences can rival, and even surpass, traditional digital channels.

Overall, the beauty sector continues to demonstrate the power of immersive experiences, albeit with mixed results. Sunsilk’s Hair Care Lab Tycoon, while experiencing a slight decline to 1.44 million visits in October, maintains impressive engagement with an average playtime of 8.6 minutes. L’Oreal Paris Catwalk Simulator shows promising growth with 1.22 million visits, though its average playtime decreased to 5.7 minutes from September’s 18 minutes.

Mobile strategies relying on mobile apps like e.l.f. Cosmetics (48,926 visits) and L’Oreal Access (4,320 visits) demonstrate significantly lower traffic than their immersive counterparts, suggesting that beauty brands are finding greater and more consistent engagement on immersive platforms.

Another breakout is Crocs World Tycoon which, despite lower visit numbers, boasts an impressive 13.4-minute average playtime—far exceeding the 3.4 minutes users spend on their mobile app.

Outlook

The October data shows several key trends that brands should consider:

1. Platform Synergy: Success increasingly depends on strategic platform choices that complement rather than compete with each other. Walmart’s strong performance across both immersive and mobile platforms exemplifies this approach.

2. Engagement Quality: While mobile apps often lead in visit numbers, immersive experiences frequently deliver longer engagement times. This suggests different platforms might serve different strategic purposes—mobile for transactions and convenience, immersive for brand building and experience.

3. Category-Specific Strategies: What works in one sector might not translate to another. Beauty brands are finding particular success with immersive experiences, while apparel brands often see stronger mobile performance.

As we move toward 2025, these trends suggest that successful digital strategies will require increasingly nuanced approaches to platform selection and experience design. Brands that can effectively balance immersive engagement with mobile convenience while staying true to their category-specific needs will likely see the strongest overall performance.

You may also like our recent report Beyond Mobile, which compared the efficacy of immersive experiences versus traditional digital strategies. Every month ALDORA aggregates the performance and engagement of major brands in immersive environments and across interactive experiences.